Top Tips for Rebuilding Credit After Debt Settlement

Rebuilding credit after debt settlement is achievable. This guide provides clear steps to help you improve your credit score and regain financial health.

Key Takeaways

Debt settlement can severely impact your credit score and remains on your report for seven years, but proactive steps can help in rebuilding.

Regularly monitoring and correcting inaccuracies in your credit reports is crucial for maintaining a favorable credit score.

Establishing a positive payment history and utilizing tools like secured credit cards and credit builder loans can significantly enhance your credit profile.

Understanding the Impact of Debt Settlement on Your Credit

Debt settlement can significantly reduce your credit score debt settlement, sometimes by 100 points or more. This substantial decline happens because settled accounts are marked on your credit report, indicating to lenders that you didn’t repay the full amount owed. The severity of the impact largely depends on various factors, such as how debt settlement affect your existing credit status and whether the debts were current or severely delinquent when settled.

Settled accounts usually remain on your credit report for seven years from the date of delinquency. This prolonged presence can pose challenges when trying to secure new credit. However, accounts marked as ‘paid-settled’ are viewed more favorably than charge-offs, which can somewhat mitigate the damage.

Comprehending how debt settlement impacts your credit is the first step toward rebuilding. Armed with this knowledge, you can take proactive measures to improve your credit score and regain financial stability.

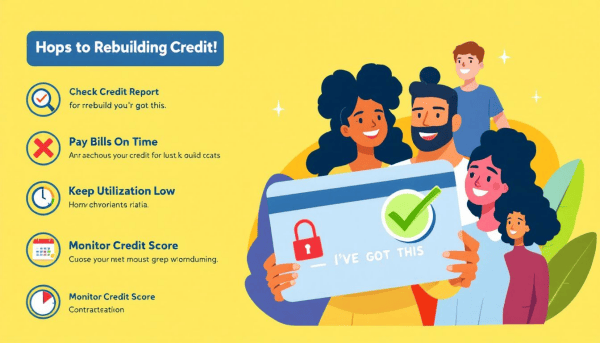

Regularly Monitor Your Credit Reports

Consistently checking your credit reports is vital for maintaining your financial health. Routinely reviewing your credit reports gives you a comprehensive view of your credit standing and highlights areas needing improvement. This proactive approach helps you stay informed about what lenders might see when evaluating your creditworthiness.

This practice also helps in spotting inaccuracies or incomplete information that might harm your credit score. Ensuring that your accounts are reported correctly can help maintain a favorable credit history and score.

Regularly checking your credit report can help you catch and dispute inaccuracies promptly, thus preventing potential damage to your credit.

Correcting Inaccuracies on Your Credit Report

Errors on credit reports are more common than you might think. These can range from incorrect personal information to accounts that do not belong to you. Correcting these inaccuracies is crucial for accurate credit reporting and maintaining a good credit score. The Fair Credit Reporting Act requires credit bureaus to investigate disputes within 30 days and notify you of their findings shortly after.

You can file disputes via mail, online, or by phone, depending on your preference and the type of error. If you provide additional information during the dispute process, the credit bureau has up to 45 days to complete their investigation.

Correcting inaccuracies on your credit report can notably improve your credit score and financial standing.

Establishing a Positive Payment History

One of the most effective ways to improve your credit score is by establishing a positive payment history. Consistent on-time payments across all your debts are crucial for enhancing your credit score. Creditors prefer to see a pattern of timely payments rather than sporadic, larger payments. This consistency demonstrates your reliability as a borrower and can significantly boost your creditworthiness.

Missed payments and missing payments can severely damage your credit score and may take years to recover from. Therefore, it’s essential to prioritize making your monthly payments on time. A consistent record of timely payments across different types of credit can enhance your overall creditworthiness and open up better financial opportunities.

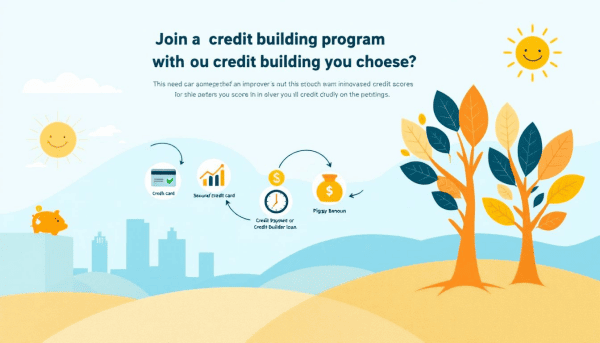

Utilizing Secured Credit Cards

Secured credit cards are a valuable tool for rebuilding credit. These cards require a cash deposit as collateral, which acts as a guarantee for the card issuer. The deposit amount typically matches your credit limit, making it a low-risk option for lenders. Secured credit cards can assist in rebuilding credit by reporting your payment history to credit bureaus, which helps improve your credit score over time.

Timely payments on secured cards can positively influence your credit report. If a payment is missed, the amount is deducted from your cash deposit, minimizing the risk for the card issuer. It’s recommended to start with one secured credit card and consider adding another after six to twelve months of positive payment history.

Successfully managing a secured credit card requires keeping balances low and making timely payments. This approach not only helps rebuild your credit but also instills good financial habits that can benefit you in the long run.

Joining a Credit Building Program

Credit building programs are subscription-based products designed to help individuals build their credit history. These programs report monthly payments to credit bureaus, which can significantly improve your credit profile over time. Many credit building programs require small, manageable monthly contributions, making them accessible to a wide range of participants.

Joining a credit building program can significantly enhance your credit scores by consistently reporting your payment history to credit bureaus. Some programs also allow participants to build savings while improving their credit, offering a dual benefit.

This structured approach to credit building can be a valuable tool in your journey to financial recovery.

Maintaining a Low Credit Utilization Ratio

A low credit utilization ratio is vital for a healthy credit score. The recommended credit utilization ratio is less than 30%. This means keeping your credit card balances low relative to your credit limits. A lower credit utilization ratio makes it easier to improve your credit score.

Closing long-held credit accounts can increase your overall credit utilization ratio, negatively impacting your credit score. Thus, keeping unused credit cards open helps maintain a higher total credit limit and lowers your credit utilization ratio.

Effective management of your credit utilization can considerably enhance your creditworthiness.

Diversifying Your Credit Mix

Having a diverse credit mix can positively impact your credit score. A varied credit profile should include both revolving credit accounts, like credit cards, and installment loans, such as mortgages or auto loans. Responsible management of different types of credit shows lenders that you are a reliable borrower.

Although a diverse credit mix only accounts for about 10% of your FICO® Score, it is still an important factor. Maintaining a balanced mix of credit types and managing them responsibly improves your credit score and showcases your financial reliability to lenders.

Keeping Old Credit Accounts Open

Keeping old credit accounts open is beneficial for your credit score. These accounts contribute positively to the length of your credit history, which is a significant factor in credit scoring. Credit bureaus favor a mix of both old and new accounts, as older accounts demonstrate responsible credit management over time.

Closing old credit cards can cause a sudden drop in your credit score. The longer you keep a credit account open, the more it benefits your credit score by providing lenders with a more comprehensive view of your credit behavior.

Keeping your older credit accounts open helps maintain a strong credit history.

Reporting Rent and Utility Payments

Reporting rent and utility payments can help improve your credit score without incurring extra debt. Rent payments can be added as an open tradeline on your credit report, which helps enhance your payment history. FICO’s newer scoring models now include reported rent payments, significantly contributing to your overall payment history.

Participating in a rent reporting service requires your landlord’s involvement to officially report your rental payments to the credit bureaus. However, mismanagement of rent payments, such as late payments or sending to collections, can negatively impact your credit report.

Consistently reporting rent and utility payments helps build a positive payment history and enhances your credit score.

Considering a Credit Builder Loan

Credit builder loans are designed to help individuals improve their credit scores by reporting consistent, timely payments to credit bureaus. These loans typically have lenient eligibility criteria, making them accessible to individuals with low or no credit scores. Additionally, they encourage savings since the loan amount is held in a savings account until repayment.

Timely payments on credit builder loans significantly affect the payment history component of your credit score, contributing about 35% to the overall score. By establishing a positive payment history through credit builder loans, you can improve your credit score over time and make it more feasible to qualify for future loans.

How Long Will It Take to Rebuild Credit?

The recovery period for credit scores after debt settlement can range from 12 to 24 months. Improvement in credit scores is generally faster for individuals who maintain other positive credit accounts. For those with a strong history of timely payments, credit repair can occur in less than six months.

Successful rebuilding often depends on timely payments and establishing new credit post-settlement. After debt settlement, the impact of negative entries on credit reports decreases over time, even though they may remain for seven years. Disputing credit report errors and reducing overall debt relative to your credit limit can also lead to an improved credit score over time.

More favorable treatment of paid-off debts by credit bureaus can aid in credit recovery. Remaining diligent and proactive can help you rebuild your credit and regain financial stability.

Should You Settle or Pay Debts in Full?

Settled debts can significantly drop your credit score, with the impact lasting on your credit report for up to seven years. Paying off debts in full usually enhances your credit score more than settling debts. If you can afford to pay your debts in full, it’s better for your overall credit health.

However, the debt settlement process may be a viable option if you are facing serious financial challenges or have substantial unsecured debt that you cannot manage. Negotiating directly with creditors can yield better outcomes for debt settlements compared to using a debt settlement company.

It’s important to weigh your options carefully and choose the best approach for your financial situation.

Avoiding Future Debt Problems

Managing debts effectively and implementing budgeting strategies can prevent future financial issues. Using debt consolidation can simplify repayment by combining loans under a single lower interest rate. Prioritizing the repayment of high-interest debts can accelerate overall debt relief and elimination.

Be cautious when choosing a debt management plan; research the legitimacy of companies offering help. Staying proactive and vigilant helps avoid debt traps and achieve financial freedom.

Summary

Rebuilding credit after debt settlement is a challenging but achievable goal. By understanding the impact of debt settlement, monitoring and correcting your credit reports, and establishing a positive payment history, you can significantly improve your credit score. Utilizing secured credit cards, joining credit building programs, and maintaining a low credit utilization ratio are all effective strategies to rebuild your credit.

Remember, the journey to financial recovery requires patience and diligence. Stay proactive, make informed decisions, and take control of your financial future. With the right approach, you can overcome the setbacks of debt settlement and achieve a good credit score once again.

Frequently Asked Questions

How does debt settlement affect my credit score?

Debt settlement can severely lower your credit score by up to 100 points or more, with this negative impact remaining on your credit report for up to seven years.

How often should I check my credit reports?

You should check your credit reports regularly to stay informed about your financial health and promptly identify any inaccuracies. Regular monitoring can help you maintain a good credit score.

What is a secured credit card, and how can it help rebuild my credit?

A secured credit card helps rebuild your credit by requiring a cash deposit as collateral and reporting your payment history to credit bureaus, thereby positively impacting your credit score over time. This makes it a practical tool for managing and improving your credit.

How long does it take to rebuild credit after debt settlement?

Rebuilding credit after debt settlement typically takes 12 to 24 months, largely influenced by your commitment to maintain positive accounts and make timely payments. Staying consistent in managing your finances will aid in a quicker recovery.

Should I settle my debts or pay them in full?

It’s generally advisable to pay debts in full to better your credit score, but if you're experiencing significant financial difficulties, a settlement may be a necessary option. Prioritize your financial well-being while considering the impact on your credit.