Top Advanced Credit Building Strategies You Should Know

Want to boost your credit score with advanced tactics? Advanced credit building strategies can guide you to a stronger financial future. This article covers key methods like diversifying credit accounts, increasing credit limits smartly, and using credit builder loans effectively.

Key Takeaways

Diversifying credit accounts, including credit cards and loans, is essential for building a strong credit profile and can enhance credit scores over time.

Strategically increasing credit limits and maintaining a low credit utilization ratio are key strategies for improving credit scores, as they demonstrate responsible credit management.

Utilizing specific tools such as secured credit cards, credit builder loans, and rent-reporting services can effectively aid individuals in building or rebuilding their credit histories.

Leverage Different Types of Credit Accounts

Diversifying your credit portfolio is one of the most effective ways to build a strong credit profile. Maintaining a variety of credit accounts, such as credit cards, installment loans, and revolving credit, can significantly enhance your credit score over time. This diversity is essential because it demonstrates to lenders and credit bureaus your ability to manage different types of credit responsibly.

A diverse mix of credit accounts not only boosts your credit score but also helps in building credit fast. Each type of credit account contributes uniquely to your credit history, showcasing your versatility in handling various financial obligations. Effectively managing these accounts paints a picture of financial reliability and stability.

Having multiple types of credit accounts showcases your ability to manage different credit obligations, which can substantially boost your credit score. For instance, becoming an authorized user on a high-limit credit card can allow you to access good credit and a positive payment history, further enhancing your credit profile.

Optimize Your Credit Mix

Optimizing your credit mix requires understanding the major types of credit accounts that impact your credit reports and scores. These include credit cards, installment loans (such as auto, mortgage, personal, and student loans), and revolving credit. Each of these types serves a unique role in building a comprehensive credit profile.

A good credit mix requires at least one type of revolving credit and one type of installment credit. This variety is beneficial because it shows lenders that you can manage different forms of credit.

For individuals with no credit history or poor credit, retail credit cards and student credit cards may be easier to obtain and can serve as a starting point for building a diverse credit portfolio.

Manage Revolving Credit Wisely

Managing revolving credit wisely is crucial for establishing a positive credit history. Revolving credit, such as credit cards, requires disciplined use to avoid the pitfalls of large balances or missed payments that can harm your credit score. Making everyday purchases with your credit card and paying your bill on time can help maintain a healthy credit profile.

Large balances or missed payments on revolving credit accounts can significantly damage your credit score. To manage revolving credit effectively, ensure that you make everyday purchases and pay your bill on time. This practice not only keeps your balances low but also demonstrates to lenders your ability to handle credit responsibly.

Strategically Increase Your Credit Limits

Increasing your credit limits strategically can play a pivotal role in improving your credit score. When you increase your credit limit, you potentially lower your credit utilization ratio, which is the proportion of your available credit that you are using. A lower credit utilization ratio is beneficial for your credit score. It contributes positively to your overall credit assessment.

Requesting a credit limit increase is a strategic move to enhance your credit profile. It’s important to approach this wisely, ensuring that you manage your spending habits responsibly. By doing so, you can enjoy the benefits of a higher credit limit without falling into the trap of increased debt.

The key is to maintain responsible spending habits after your credit limit is increased. This means avoiding the temptation to ramp up your credit card spending, which could negate the benefits of a higher limit. Keeping your credit utilization low remains essential to maintaining a good credit score.

Timing Your Requests

Timing your requests for a credit limit increase is crucial for maximizing your chances of approval. Request an increase after demonstrating responsible credit use over some time. Typically, the optimal time to seek a credit limit increase is six months after opening the account.

Demonstrating responsible credit management, such as making on-time payments and maintaining low balances, can significantly enhance your chances of getting a credit limit increase approved. This approach shows lenders that you are a low-risk borrower, making them more likely to grant your request.

Preparing for Approval

Preparing for approval of a credit limit increase involves several key steps. First, ensure that your account is in good standing, with no missed payments or high balances. Accounts that are paid off or have a low balance tend to increase the likelihood of credit limit approval.

Before requesting a credit limit increase, it’s beneficial to pay down existing debt. This not only improves your credit utilization ratio but also demonstrates to lenders your commitment to responsible credit management.

After getting approved, avoid increasing your spending to maintain a good standing.

Utilize Secured Credit Cards Effectively

Secured credit cards are powerful tools for building or rebuilding credit. These cards require a security deposit for approval, which then serves as your credit limit. Examples include the Discover it® Secured Credit Card and the Blue Cash Preferred® Card from American Express, both designed to help build credit.

Using secured credit cards effectively requires patience and discipline. Track your progress regularly to see how your credit score improves over time. This methodical approach ensures that you stay on the right path towards building a solid credit history.

Utilizing secured credit cards effectively can pave the way for transitioning to unsecured cards, which offer more benefits and higher credit limits. This transition, however, requires responsible use and a strong track record of on-time payments.

Choosing the Right Secured Card

Selecting the right secured credit card is key for building your credit history. Choose a card that reports to all three major credit bureaus. This ensures that your positive payment history is reflected in your credit reports, boosting your credit score.

Typically, secured credit cards require a security deposit that serves as your credit limit. The minimum deposit is usually around $200, though some cards may offer lower deposit options. Make sure to choose a card that fits your financial situation and credit-building goals.

Transitioning to Unsecured Cards

Transitioning from secured to unsecured credit cards is a significant milestone in your credit-building journey. Responsible use of your secured card can lead to the issuer reviewing your account and potentially raising your credit limit or transitioning you to an unsecured card.

Facilitate this transition by maintaining a record of on-time payments and low credit utilization. This responsible behavior not only helps build a good credit history but also increases your chances of being approved for an unsecured card with better terms and higher limits.

Take Advantage of Credit Builder Loans

Credit builder loans are specifically designed to help individuals with limited or poor credit history build credit. These loans are a low-cost option that can significantly improve your credit standing when used correctly. Payments on credit builder loans are reported to credit bureaus, reflecting positively on your credit report.

The primary purpose of a credit builder loan is to help you build or rebuild your credit. Timely payments on these loans can positively impact your credit score, demonstrating to lenders your ability to manage debt responsibly. This can be particularly beneficial for those who have struggled with credit in the past.

Credit builder loans often have lenient acceptance criteria, making them accessible to individuals with poor or no credit history. After paying off the loan, you gain access to the funds, and your timely payments positively impact your credit score.

Finding the Best Credit Builder Loans

Credit unions and community banks are common sources for obtaining credit builder loans. Ensure the lender reports to all three major credit bureaus when selecting a credit builder loan. This ensures that your positive payment history is accurately reflected in your credit reports.

Additionally, some credit builder loans, such as those offered by Self, have low monthly payment options starting at $25. This makes them an affordable option for those looking to build their credit without a significant financial burden.

Maximizing Loan Benefits

Maximizing the benefits of credit builder loans involves making timely payments and setting up automatic payments to ensure consistency. These loans are designed to help you establish or improve your credit scores by reporting your payment history to the credit bureaus.

Since the funds from a credit builder loan are typically not accessible until the loan is fully repaid, it encourages disciplined financial behavior. This structure not only helps in building credit but also instills good financial habits that can benefit you in the long run.

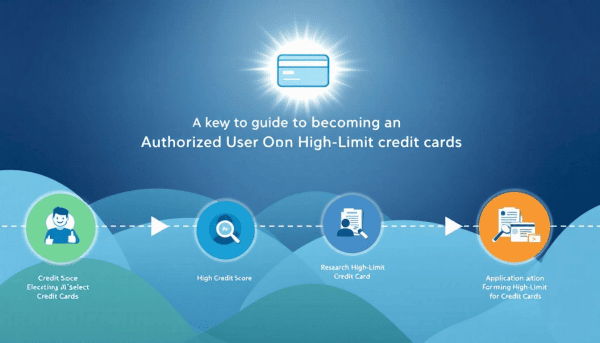

Become an Authorized User on High-Limit Credit Cards

A swift way to establish a positive credit history is by becoming an authorized user on a high-limit credit card. Many credit card issuers report the entire account history to the credit bureaus, allowing you to benefit from the primary cardholder’s good credit behavior. This can be especially beneficial if you are new to credit or looking to rebuild your credit profile.

The primary cardholder must add you to their credit card account, which then appears on your credit reports. This addition can significantly enhance your credit score, provided the primary cardholder maintains a positive credit history.

However, it’s crucial to select the right primary cardholder to avoid any potential negative impacts. If the primary cardholder mismanages the account, it could harm your credit score instead of helping it.

Selecting the Right Primary Cardholder

Choosing a primary cardholder with a strong credit history and consistent payment behavior can significantly enhance the benefits of being an authorized user. A primary cardholder with a positive credit history can lead to better terms and higher credit limits for the authorized user.

However, if the primary cardholder overspends or pays late, it could harm your credit. Therefore, it’s essential to select someone who manages their credit responsibly.

Monitoring Your Impact

Monitoring your credit reports regularly is crucial to track the impact of being an authorized user. Becoming an authorized user on someone else’s high-limit credit card can help boost your credit history by providing you with a credit account without the responsibility of making payments.

You can obtain free credit reports from each of the three major credit bureaus annually to keep track of your credit accounts and any changes. If you notice that being an authorized user is not positively affecting your credit score or if the primary cardholder misses payments, it may be wise to consider removing yourself from that account.

Report Rent and Utility Payments

Rent and utility payments are often overlooked as tools for building credit. Typically, these payments do not automatically build credit, but using rent-reporting services can add them to your credit reports. This can provide a quick boost to your credit score.

Paying your monthly bills on time improves your credit score and establishes a positive credit history. Using services like Experian Boost, which allows you to add utility and telecom payments to your credit report, can further enhance your credit profile.

Paying rent and utility bills on time and reporting these payments can help you build a stronger credit history without taking on additional debt.

Using Rent-Reporting Services

Rent-reporting services allow landlords to report tenant payments to credit bureaus, helping build a positive credit history. To sign up for these services, tenants should check if their landlord offers it or use a third-party service.

Using rent-reporting services can improve credit scores by including regular rent payments in your credit history. This addition can be particularly beneficial for those with limited credit histories.

Adding Utility Payments via Experian Boost

Experian Boost allows users to report utility and cell phone bills to enhance their credit profile. The utility payments reported through Experian Boost can increase your credit report’s data points by including cell phone and utility bills.

On average, users see a credit score increase of 13 points by using Experian Boost to report their utility payments. This can be a simple and effective way to improve your credit scoring without taking on new debt.

Regularly Monitor Your Credit Reports

Regular monitoring of your credit reports is crucial to ensure your credit-building efforts are effective. Checking your credit reports can reveal inaccurate or incomplete information that might affect your credit scores. If you find inaccuracies, dispute them promptly to maintain the accuracy of your credit history.

Consistent monitoring keeps you on top of your credit profile and allows for corrective action when necessary. Regularly reviewing your credit reports helps you spot potential issues early, allowing you to address them before they impact your credit score.

Accessing Free Credit Reports

Individuals can check their credit reports for free once a year from each of the three major credit bureaus through AnnualCreditReport.com. Many banks provide free access to credit reports. This is typically available at least once a year.

Accessing free credit reports is essential for maintaining a healthy credit profile and monitoring your financial health. Frequent checks ensure your credit history remains accurate and up-to-date.

Disputing Credit Report Errors

To dispute an error on your credit report, notify the credit bureau of the inaccuracies you’ve identified. You can submit a dispute online, by mail, or over the phone.

After submitting a dispute, the credit bureaus will investigate the error by contacting the creditor. Ensuring your credit report is accurate helps maintain a positive credit history and improves your credit score.

Maintain a Low Credit Utilization Rate

The credit utilization ratio shows the proportion of credit you’re using relative to your total available credit. This ratio is a significant factor that affects your credit score.

Maintaining a low credit utilization rate is crucial for building credit. The recommended credit utilization ratio to maintain is below 30%. Keeping this ratio low demonstrates responsible credit management and positively impacts your credit score.

Requesting a higher credit limit can lead to a lower credit utilization ratio, enhancing your credit score. This strategy helps you maintain a lower utilization rate even if you have to carry a balance occasionally.

Calculating Your Credit Utilization

To find your credit utilization rate, sum your credit balances and divide by your total credit limits, then multiply by 100. This calculation gives you the percentage of your available credit that you are using.

Managing your credit utilization effectively is critical because it can significantly affect your credit score. Keeping it below 30% is generally recommended for maintaining a good credit score.

Strategies for Reducing Utilization

Consider requesting a credit limit increase or opening multiple cards to lower your credit utilization ratio. To quickly improve your credit score, focus on paying down the credit card with the highest utilization ratio. This strategy can have an immediate positive impact.

Utilizing these methods effectively can enhance your overall credit score and reduce financial stress. Lowering your credit utilization is crucial for improving your credit score and maintaining financial health.

Make Consistent On-Time Payments

Repayment history constitutes up to 35% of a credit score, making timely payments crucial. On-time payments are the most significant factor in building a strong credit score. Maintaining a good payment history with a secured credit card is essential as it significantly influences your credit score. Demonstrating a consistent record of on-time payments significantly boosts your chances of securing a credit limit increase.

Setting up automatic payments can help ensure you never miss a due date, thereby protecting your credit score. Making payments on time and paying at least the minimum to maintain a good credit score is crucial.

Setting Up Automatic Payments

Automatic payments ensure bills are paid on time, reducing the risk of missed due dates. This approach helps maintain a positive credit history and prevents late or missed payments from harming your credit score.

By setting up automatic payments, you can ensure that your monthly bills are paid on time without the hassle of remembering due dates.

Prioritizing Debt Payments

When managing debts, focus on paying off high-interest debts first to optimize credit score improvement. This approach reduces the overall interest you pay and frees up more funds to pay down other debts.

Prioritizing high-interest debt can quickly improve your credit score and reduce financial stress. By focusing on these debts first, you can achieve a more manageable debt load and a healthier credit profile.

Summary

In summary, building a strong credit profile requires a multifaceted approach. By leveraging different types of credit accounts, strategically increasing your credit limits, utilizing secured credit cards, taking advantage of credit builder loans, and becoming an authorized user, you can significantly enhance your credit score. Additionally, reporting rent and utility payments, regularly monitoring your credit reports, maintaining a low credit utilization rate, and making consistent on-time payments are essential strategies for maintaining and improving your credit.

By implementing these advanced credit-building strategies, you can unlock financial opportunities and achieve greater financial stability. Stay disciplined, monitor your progress, and make informed decisions to build and maintain a robust credit profile.

Frequently Asked Questions

What is the best way to start building credit if I have no credit history?

The best way to start building credit with no history is to open a secured credit card and ensure timely payments. Also, consider becoming an authorized user on a trusted individual's high-limit card and explore credit builder loans to further establish your credit profile.

How can I improve my credit score quickly?

To improve your credit score quickly, ensure all payments are made on time, keep your credit utilization low, and dispute any inaccuracies on your credit reports. Additionally, consider using services like Experian Boost to report utility payments for an extra lift.

What is a good credit utilization ratio to maintain?

Maintaining a credit utilization ratio below 30% is advisable, as it reflects responsible credit management and can enhance your credit score.

Can rent payments help build my credit?

Yes, rent payments can help build your credit if reported through rent-reporting services, thus contributing positively to your credit history and improving your credit score.

How often should I check my credit reports?

You should check your credit reports at least once a year from each of the three major credit bureaus to identify inaccuracies and maintain a healthy credit profile. Regular monitoring is essential for effective credit management.