Top 7 Credit Myths Debunked for Better Financial Health

Curious about common credit myths? In this article, we debunk the top 7 credit myths debunked to help you better understand your financial health.

Key Takeaways

Checking your own credit score does not lower it, as it is a ‘soft inquiry’ that has no impact.

Carrying a balance on credit cards can harm your credit score; maintaining low utilization and paying in full is more beneficial.

Payment history and credit utilization drive your credit score; income and debit card use have no direct impact. However, during a credit application, lenders evaluate additional factors such as income and credit history. It's important to note the difference between hard and soft inquiries: a hard inquiry may affect your credit score, while checking your own credit does not.

Understanding Credit Scores

What are Credit Scores and How are They Calculated?

Credit scores are three-digit numbers that represent your creditworthiness, essentially indicating how likely you are to repay borrowed money. The most widely recognized credit scoring model is the FICO score, which ranges from 300 to 850. Generally, a good credit score is considered to be 700 or higher.

Credit scores are calculated by credit bureaus like Equifax, Experian, and TransUnion. These bureaus gather information from your credit report, which includes details about your credit accounts, payment history, and credit utilization ratio. The credit scoring model evaluates this information based on five main categories:

Payment History (35%): This is the most significant factor and includes on-time payments, late payments, and accounts sent to collections.

Credit Utilization Ratio (30%): This measures the amount of credit you’re using compared to your total credit limit. Keeping this ratio below 30% is ideal.

Length of Credit History (15%): This considers the age of your oldest account and the average age of all your accounts.

Types of Credit Used (10%): A mix of different credit types, such as credit cards, installment loans, and mortgages, can positively impact your score.

New Credit (10%): This includes new accounts, inquiries, and recent credit applications.

Understanding how credit scores are calculated can help you take proactive steps to improve your score. Focus on maintaining a good payment history, keeping your credit utilization low, and managing a diverse mix of credit accounts responsibly.

Myth: Checking Your Credit Score Lowers It

One of the most pervasive myths about credit is that checking your credit score will lower it. This belief often prevents people from regularly monitoring their financial health. Checking your own credit score is a “soft inquiry.” This means that it does not have any impact on your credit score.

Soft inquiries, such as checking your own credit score, do not impact your score and are not visible to lenders. In contrast, “hard inquiries” occur when you apply for loans or credit cards, which can temporarily lower your score. Regularly monitoring your credit report is crucial for identifying and disputing inaccuracies, ensuring that your financial health remains intact.

Regularly reviewing your credit reports allows you to track progress and make informed decisions. Staying proactive helps maintain a healthy credit score and avoid potential financial pitfalls.

Myth: Carrying a Balance on Your Credit Card Boosts Your Credit Utilization Ratio

Another common myth is that carrying a balance on your credit card will boost your credit score. In reality, carrying a balance can hurt your credit score and lead to unnecessary interest charges. This misconception often leads people to accumulate debt, thinking it will benefit their credit.

The key to a healthy credit score lies in maintaining a low credit utilization ratio, ideally below 30%. This means using only a small portion of your available credit. By paying off your credit card balance in full each month, you avoid interest charges and demonstrate responsible credit behavior.

Remember, it’s not the balance you carry but how you manage your credit that matters. Paying off your balances promptly is the best way to keep your credit score in good shape and avoid the pitfalls of high-interest debt.

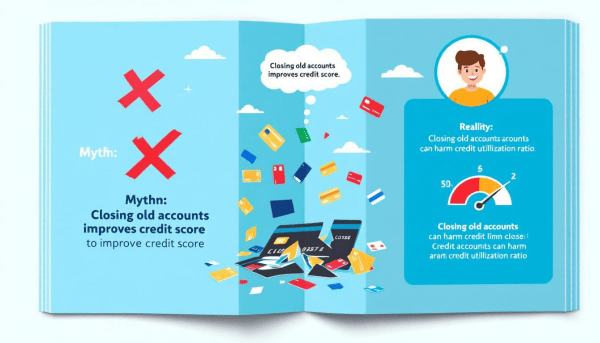

Myth: Closing Credit Cards Improves Your Credit Score

Many believe that closing unused credit cards will improve their credit score. However, this can actually hurt your credit score by increasing your credit utilization ratio. When you close a credit card, you reduce your available credit, which can make your existing balances constitute a larger percentage of your total credit limit.

Maintaining unused credit cards contributes to a greater amount of available credit, which is beneficial for your score. Keeping credit cards open, particularly those without annual fees, is beneficial for maintaining a favorable credit utilization ratio.

Instead of closing credit accounts, focus on managing them responsibly. Keep your credit card accounts open and use them occasionally to keep them active, which can help maintain a healthy credit score.

Myth: My Income Impacts My Credit Score

A prevalent myth is that your income directly impacts your credit score. Though income is assessed during credit applications, it doesn’t impact your credit score. Credit scores are determined by payment history and amounts owed, not by income or other demographics.

A high income doesn’t guarantee a good credit score, nor does a low income doom you to a bad one. Your credit score is influenced by your credit utilization and payment history, making these aspects more significant than your income level.

Good credit habits, like timely payments and wise debt management, are essential for a strong credit score, regardless of income. Concentrating on these practices helps build and maintain a healthy credit profile.

Myth: A Good Credit Score Means You're Rich

Another widespread misconception is that a high credit score means you’re wealthy. In truth, a good credit score indicates that you are perceived as a lower risk by lenders, not necessarily that you have a high income or substantial wealth.

A good credit score reflects responsible credit behavior, such as making timely payments and keeping credit card balances low. Even individuals with limited financial resources can achieve a good credit score through responsible credit scoring usage.

The notion that only the wealthy have high credit scores is incorrect. Anyone can achieve and maintain a good credit score through responsible credit management and sound financial decisions.

Myth: Paying Off Debt Increases Your Credit Score

It’s often believed that simply paying off debt will automatically increase your credit score. While paying off credit card debt can improve your credit score by reducing your credit utilization, paying off installment debts like car loans might not have the same effect.

Installment loans, such as mortgages and student loans, can positively contribute to building a credit score when managed responsibly. Clearing these debts demonstrates financial responsibility but won’t necessarily boost your score immediately.

The key is to manage all types of debt wisely. Reducing credit card balances can have a significant positive impact, while paying off installment loans reflects long-term financial health.

Myth: Employers Can See Your Credit Score

A common myth is that employers can see your credit score. In reality, they do not have access to your credit score but can view a limited version of your credit report. Employers check credit histories to evaluate candidates’ financial responsibility and trustworthiness.

Regular monitoring of your credit reports is essential to verify accuracy and detect potential identity theft. Errors on your credit report can be disputed directly with the credit bureau or the involved lender, and a credit check can help ensure everything is in order.

Understanding what employers can and cannot see helps you take the right steps to maintain a clean credit history and address any issues that might arise.

Myth: Getting Married Will Merge My Credit Score with My Spouse

Many believe that getting married will merge their credit scores with their spouse’s. However, marriage does not influence individual credit scores or credit histories. Each partner retains their own credit score even after marriage.

Joint accounts can impact both partners’ credit scores due to shared financial activity. Responsible communication and management of joint finances are essential to maintain healthy credit profiles for both partners.

Recognizing that marriage doesn’t merge credit scores helps couples manage finances more effectively and avoid confusion.

Myth: Using Debit Cards Helps Build a Good Credit Score

A common belief is that using debit cards can help build a good credit score. However, only credit card activity is reported to credit bureaus and influences your credit score. Debit card transactions do not establish credit since funds are withdrawn directly from a checking account without any borrowing. Therefore, using debit cards has no impact on your credit score.

Building a good credit score requires responsible credit card use and timely payments. While convenient, debit card usage does not contribute to your credit history.

Myth: All Debt Is the Same

It’s a common myth that all debt is the same. In reality, revolving credit accounts, like credit cards, differ significantly from installment loans, such as car loans. Managing different types of debt can showcase financial responsibility and help improve your credit score.

Having a mix of credit types, such as mortgages, car loans, and student loans, can enhance your credit profile. Understanding how different types of debt impact your credit helps manage finances more effectively and improves overall credit health.

Credit Bureaus and Credit Reports

How Credit Bureaus Collect and Use Credit Information

Credit bureaus play a crucial role in the credit scoring process by collecting and maintaining credit information from various sources. These sources include credit card issuers, banks, mortgage lenders, collection agencies, and public records. The information gathered is used to create your credit report, which contains comprehensive details about your credit history.

Your credit report includes:

Credit Accounts: Information about your credit cards, loans, and mortgages.

Payment History: Records of on-time payments, late payments, and accounts sent to collections.

Credit Utilization Ratio: The amount of credit you’re using compared to your total credit limit.

Credit Inquiries: Requests for your credit report from lenders and creditors.

Public Records: Information about bankruptcies, foreclosures, and tax liens.

Credit bureaus provide these credit reports to lenders, creditors, and other authorized parties, who use the information to evaluate your creditworthiness and make lending decisions. Understanding how credit bureaus collect and use your credit information can help you manage your credit more effectively.

How to Check and Correct Errors on Your Credit Report

Regularly checking your credit report is essential to ensure it’s accurate and up-to-date. You can request a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year through AnnualCreditReport.com. Here’s how to do it:

Request Your Free Credit Report: Visit AnnualCreditReport.com and request a free credit report from each credit bureau.

Review Your Credit Report: Carefully review your credit report for any errors or inaccuracies. Look for incorrect account information, payment history errors, or unfamiliar accounts.

Dispute Errors: If you find an error, contact the credit bureau to dispute it. Provide documentation to support your dispute, such as payment records or identification.

Follow Up: The credit bureau will investigate your dispute and correct any errors if necessary. Follow up to ensure the corrections are made.

Correcting errors on your credit report can help improve your credit score and ensure that lenders and creditors have accurate information when evaluating your creditworthiness. Regular monitoring and timely corrections are key to maintaining a healthy credit profile.

Summary

Summarizing the key points from each myth debunked will reinforce the importance of understanding how credit works. Emphasize that myths around credit scores often lead to poor financial decisions and highlight the essential facts uncovered.

Encourage readers to apply these insights to manage their credit wisely, emphasizing the importance of regular monitoring and responsible credit usage.

Inspire readers to take control of their financial future with accurate credit knowledge, dispelling myths that have held them back.

Frequently Asked Questions

Does checking my credit score hurt my score?

Checking your own credit score does not hurt your score, as it is considered a soft inquiry. You can monitor your credit without any negative impact on your overall score.

Will carrying a balance on my credit card help my score?

Carrying a balance on your credit card will hurt your credit score and result in additional interest charges. It's best to pay off your balance in full each month to maintain a healthy credit profile.

Do employers have access to my credit score?

Employers do not have access to your credit score; however, they can view a limited version of your credit report during the hiring process. This information may include your credit history and public records, but not your actual score.

Will getting married merge my credit score with my spouse's?

No, marriage does not combine your credit scores; each person's credit history remains separate. It's essential to manage your individual finances responsibly.

Can using debit cards help build my credit score?

Using debit cards will not help you build your credit score since their activity is not reported to credit bureaus. To improve your credit score, consider using credit cards responsibly.