Does Credit Monitoring and Debt Consolidation Affect Your Credit Score?

Curious about how credit monitoring and debt consolidation can affect your credit score? This article will explain how monitoring your credit can help you manage your finances and how debt consolidation can simplify your debt repayment strategy. You’ll learn what to expect, including potential risks and long-term benefits.

Key Takeaways

Credit monitoring is essential for tracking changes in credit reports and understanding credit health, aiding timely decision-making for financial strategies.

Debt consolidation simplifies debt management by combining multiple debts into one loan, though initial impacts on credit scores should be carefully considered.

To minimize negative effects of debt consolidation on credit scores, maintain old credit accounts, manage credit utilization, and ensure timely repayments.

Understanding Credit Monitoring

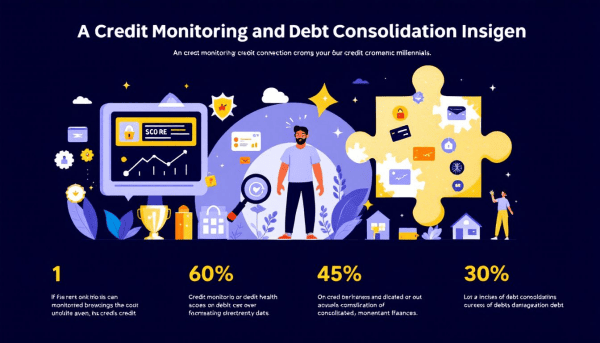

Credit monitoring is akin to having a vigilant financial watchdog. These services meticulously track alterations in your credit reports and notify you about significant changes, such as new credit accounts, hard inquiries, or changes in credit card balances. This vigilance keeps you informed about your credit health, enabling prompt action if issues arise.

Credit monitoring services provide essential tools such as your FICO Score, Experian credit report, and real-time alerts. This means you can see how various activities, like opening a new credit account or paying down debt, impact your credit scores in real time. Grasping these dynamics enables better decision-making regarding your financial strategies.

Regularly checking your credit report clarifies how different factors affect your credit scores. You can select from different credit monitoring solutions based on your specific needs and preferences, ensuring that you have the right level of oversight for your financial situation. This proactive approach to credit management is invaluable in maintaining a healthy credit profile.

Debt Consolidation Explained

Debt consolidation is a strategy designed to simplify your financial life by combining multiple debts into a single loan. This approach often involves taking out a debt consolidation loan to pay off existing debts, which can include credit card balances, auto loans, and personal loans. By consolidating debt, you reduce the hassle of managing multiple payments and can potentially secure a lower interest rate. Additionally, many individuals seek to consolidate debt to improve their overall financial health.

Personal loans, balance transfer credit cards, and home equity loans are common methods for debt consolidation. Each option offers different terms and conditions suitable for various financial situations. Each method has its advantages, and the choice largely depends on your financial situation. For instance, personal loans generally require a good credit history to qualify for the best rates, while home equity loans offer lower interest rates due to the collateral value of your home.

Debt consolidation effectiveness varies by individual circumstances. A strong credit history might secure lower interest rates with consolidation loans, but consider risks like using your home as collateral for a home equity loan. Debt consolidation hurt can occur if these risks are not carefully evaluated.

Recognizing these nuances aids in making informed decisions and consolidating debt effectively.

How Credit Monitoring Supports Debt Consolidation

Credit monitoring plays a pivotal role in the debt consolidation process. Monitoring your credit score helps pinpoint the best time for debt consolidation. Checking your credit health before applying for a consolidation loan helps you understand your current standing, potentially securing better loan terms.

Once you’ve consolidated your debts, credit monitoring helps you track your progress. It allows you to see if your debt management strategy is effective, ensuring that your efforts are reflected positively in your credit scores. This ongoing oversight is crucial, especially when you’re working towards improving your financial health.

Credit monitoring services offer insights into your credit health and notify you of new hard inquiries. Staying informed helps you manage your credit utilization ratio, which can notably improve your credit score post-consolidation. Timely payments on your debt consolidation loan or balance transfer credit card can further enhance your credit score over time.

The Initial Impact on Your Credit Score

The initial impact of debt consolidation on your credit score can be a mixed bag. When you apply for a new consolidation loan, a hard inquiry is made on your credit report, which can temporarily reduce your credit score by 5 to 10 points. While this dip is usually short-lived, it’s something to be aware of as you begin the debt consolidation process.

Debt consolidation impacts your credit utilization ratio, a key component of your credit score. By paying off high-balance credit cards, you can lower your credit utilization, potentially boosting your credit score. However, if you close credit card accounts after consolidating debt, it can reduce your available credit, negatively impacting your credit score.

Opening a new loan account can reduce the average age of your credit accounts, potentially lowering your credit scores. Although discouraging, these initial effects are usually temporary. Diligent management and timely payments can help your credit score recover and improve over time.

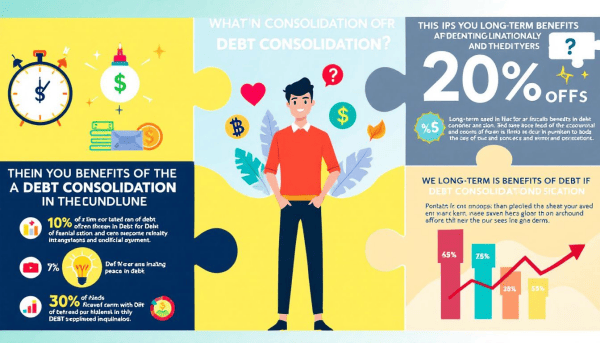

Long-Term Benefits of Combining Multiple Debts

While the initial impact on your credit score might be concerning, the long-term benefits of debt consolidation are substantial. Combining multiple debts into a single loan simplifies your financial management, leading to improved credit health. This streamlined approach reduces the risk of missed payments and helps you stay on top of your finances.

Debt consolidation can also significantly improve your credit utilization ratio. By transferring credit card debt to a personal loan, you can reduce your overall credit utilization, positively affecting your credit scores. Regularly monitoring your credit can help you manage this ratio, ensuring that your consolidation efforts yield the desired results.

Consolidation-driven debt repayment boosts your payment history, a crucial factor in credit scoring. Lower interest rates from consolidation can ease the burden of payments, making it easier to maintain on-time payments and avoid additional debt. Although the initial dip in credit score might be a deterrent, the long-term benefits make debt consolidation a worthwhile strategy.

Strategies to Minimize Negative Impacts

Minimizing debt consolidation’s negative impacts requires specific strategies. First, keep old credit accounts open to maintain the length of your credit history. Keeping these accounts open helps maintain a longer credit history, which is beneficial for your credit score.

Avoiding new credit accounts for a while helps maintain your credit history length and manage your debt utilization ratio. Being diligent with your repayment plan and making payments on time is critical to avoid hurting your credit scores post consolidation.

Following these strategies helps mitigate adverse effects and maintain a healthy credit profile.

Choosing the Right Debt Consolidation Method

Selecting the appropriate debt consolidation method is vital for effective debt management. Employing the right strategy guides the consolidation process effectively. Your credit reports and credit scores are key factors in determining whether you qualify for a debt consolidation loan and what interest rates you might receive.

If traditional debt consolidation methods seem unappealing, exploring alternatives could be beneficial for managing debt effectively. Understanding the pros and cons of each method and how they fit your financial situation is crucial.

Personal Loans

A personal loan is a popular option for debt consolidation. This type of loan provides a lump sum to pay off debts, which is then repaid in monthly installments over a period of months or years. The interest rates on personal loans are typically fixed, offering stability as the rates do not change during the loan’s life.

A debt consolidation loan, which is a form of a personal loan, allows you to consolidate credit card debt with lower interest rates and better terms. This can simplify your finances by reducing multiple payments into one monthly payment, making it easier to manage your debt. Additionally, debt consolidation loans can provide a structured approach to paying off your obligations.

Balance Transfer Credit Cards

Balance transfer credit cards are another effective method for consolidating debt. These cards often come with an introductory APR period as low as 0 percent for 12–18 months, making it an ideal time to pay off existing debt without accruing additional interest.

However, balance transfers usually incur a fee of 3 to 5 percent of the transferred amount. Despite this fee, the savings from reduced interest can make this an attractive option for consolidating multiple debts.

Home Equity Loans

Home equity loans offer another avenue for debt consolidation. These loans allow homeowners to borrow against their property, using the home as collateral. The primary benefit of home equity loans is the lower interest rates compared to unsecured loans.

Repayment terms for home equity loans can be longer, which may increase overall costs despite the lower interest rates. This method can be advantageous for those with significant equity in their homes, providing a substantial loan amount at a lower cost.

Monitoring Your Credit Post-Consolidation

Post-consolidation credit monitoring is crucial for assessing your debt management strategy’s effectiveness. Timely payments on a consolidation loan consistently enhance your payment history, a critical credit scoring factor. Staying informed about your credit score can motivate you to adhere to your repayment plan.

Regular credit report checks help you quickly identify and correct any errors post-debt consolidation. Credit monitoring can detect unauthorized activities early, protecting against identity theft and maintaining your financial health.

Monitoring your credit closely allows you to track the impact of debt consolidation on your credit health, ensuring positive financial outcomes.

When to Consider Professional Help

There are times when professional help is necessary to manage debt effectively. Struggling with minimum credit card payments or a debt-to-income ratio over 40% are clear signs to seek professional help. Using credit cards for essential expenses and experiencing significant financial stress are also warning signs that professional assistance is needed.

Debt management plans can offer lower payments without taking out a new loan but may restrict opening new credit accounts. A financial advisor or credit counseling agency can offer personalized advice and strategies for more effective debt management.

If considering debt settlement or bankruptcy, professional advice is crucial to understand potential credit score impacts and long-term effects.

Summary

In summing up, credit monitoring and debt consolidation are powerful tools that can significantly impact your financial health. Understanding how to use these tools effectively can help you manage your credit scores better and achieve financial stability. Combining multiple debts into a single loan simplifies financial management and can lead to long-term improvements in your credit health.

While there may be initial impacts on your credit score, the long-term benefits of debt consolidation are substantial. By choosing the right consolidation method and employing strategies to mitigate negative effects, you can maintain a healthy credit profile. Embrace these strategies and take control of your financial future today.

Frequently Asked Questions

Will debt consolidation hurt my credit score?

Debt consolidation may initially lower your credit score due to hard inquiries and alterations in credit utilization. However, managing your payments responsibly can lead to an improvement in your score over time.

What are the best debt consolidation methods?

The best debt consolidation methods are personal loans, balance transfer credit cards, and home equity loans, with the most suitable choice depending on your financial situation and credit history. Assessing these factors will help you determine the optimal method for consolidating your debts.

How can credit monitoring help with debt consolidation?

Credit monitoring is essential for tracking your credit score and identifying the optimal time for debt consolidation, while also enabling you to monitor your progress afterward. Utilizing these insights can lead to more informed financial decisions and improved credit health.

What should I avoid to minimize negative impacts on my credit score?

To minimize negative impacts on your credit score, avoid closing old credit accounts, opening new accounts frequently, and making late payments. Maintaining long-standing credit lines and ensuring on-time payments are essential for sustaining your credit health.

When should I consider professional help for debt management?

Consider professional help for debt management if you are struggling to make minimum payments, have a high debt-to-income ratio, or find yourself relying on credit cards for essential expenses. Seeking guidance can help you implement tailored strategies for effective debt management.