Best Dispute Reason for Collections on Credit Report: A Clear Guide

Struggling with collections on your credit report? Finding the best dispute reason for collections on credit report can make a significant difference in improving your credit score. This guide will help you identify the most effective dispute reasons and how to benefit from them.

Key Takeaways

Understand how collections affect your credit score and take action to dispute inaccuracies to improve your financial health.

Common reasons to dispute collections include billing errors, identity theft, undelivered services, and incorrect account information.

Gather strong evidence, including relevant documents and communication records, to support your disputes effectively and protect your credit report.

Understanding Collections on Credit Reports

When a debt is sent to collections, it is recorded on your credit report, signaling that the account is in default. This record, detailing both paid and unpaid debts, provides significant data that influences your credit scores. The impact of these collections on your credit score can vary based on factors such as the total amount owed and your payment history.

Debt collections generally have a negative effect on credit scores, impacting aspects such as payment history. Credit scoring algorithms use these events to evaluate creditworthiness. Settling a debt can lead to more favorable treatment in credit scoring models, even if the collection record remains for seven years. Grasping the influence of these collections on your credit is key to steering your way to financial recovery.

Being aware of the impact of collections on your creditworthiness empowers you to manage your credit report effectively, correct errors, and take steps to enhance your financial health. Let’s examine the common reasons to dispute collections and how to use them to your benefit.

Common Reasons to Dispute Collections

Correcting inaccurate collections is vital for maintaining credit health and preventing negative effects on credit scores. Disputes can arise from assertions that debts are not owed or that the information is inaccurate. Billing errors are a common reason for disputing a collection. Additionally, contractual disputes and unauthorized charges can also lead to disputes. These disputes are considered legitimate when they arise from disagreements over debt claims.

Disputing a collection involves challenging the debt valid claim made by the creditor or collection agency and a credit agency. Validating disputes can enhance consumers’ credit reports and financial standing.

Common reasons for disputing collections include billing errors, identity theft, undelivered services, and incorrect account information.

Billing Errors

Billing errors occur when there are mistakes in the amounts charged or in the services billed, leading to incorrect collections. Disputing a collection due to billing errors is legitimate as it helps protect your credit report from inaccuracies. Regularly reviewing your bills and bank statements helps catch billing errors early before they escalate.

Not disputing billing errors can lead to long-term credit score damage and financial stress. Promptly addressing these errors helps maintain an accurate credit report and avoid unwarranted financial burdens.

Let’s move on to another common reason for disputing collections: identity theft.

Identity Theft

Victims of identity theft often find themselves facing collections for debts they never incurred. If you suspect identity theft, report the incident to the authorities and dispute the fraudulent debts with credit bureaus. In most cases, victims may receive collection notices for debts that are not theirs.

Addressing these fraudulent debts quickly can prevent further damage to your credit report. Swift action protects your financial health and ensures your credit report accurately reflects your true credit history.

Now, let’s discuss another valid reason for disputing collections: services not rendered.

Service Not Rendered

Charges for services that were agreed upon but not delivered can be valid grounds for disputing collections. If services promised were not delivered, disputing charges ensures your credit report remains accurate and reflects only genuine debts.

Disputing charges for undelivered services improves credit report accuracy and upholds consumer rights. By challenging these incorrect charges, you protect yourself from paying for services never received and maintain a healthy credit report.

Next, we’ll examine how incorrect account information can lead to wrongful collections.

Incorrect Account Information

Errors in personal information or account numbers can result in wrongful collections. Promptly addressing these inaccuracies prevents damage to your credit report and may involve contacting a credit reporting agency.

Addressing mistakes in personal or account details immediately helps maintain the accuracy of your credit report, ensuring it accurately reflects your financial history.

Now that we understand the common reasons for disputing collections, let’s explore how to gather evidence for your dispute.

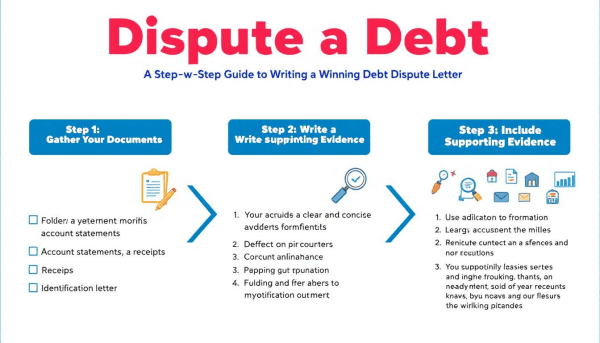

How to Gather Evidence for Your Dispute

Verifying the accuracy of debt details is the first step in gathering evidence for your dispute. Collect relevant information, records, and documents to substantiate your claims. Check all agreements and related documents to verify the accuracy of the claimed debt.

Gather evidence that supports your case and proceed with the dispute if the claimed debt is incorrect. A well-structured dispute letter should clearly state the reasons for contesting the debt and include supporting evidence.

Let’s break down the process of gathering evidence into three main steps: collecting relevant documents, maintaining communication records, and obtaining witness statements.

Collect Relevant Documents

Relevant documents include bills, contracts, and any written communication related to the disputed debt. Bills and contracts serve as essential evidence in substantiating your dispute claims against collection listings. These documents can provide proof of billing mistakes, erroneous data entry, or miscommunication that caused the dispute.

Collecting these documents helps build a strong case to dispute the debt and ensures that your credit report accurately reflects your financial history. Now, let’s discuss the importance of maintaining communication records.

Maintain Communication Records

Keeping records of communications with creditors or collection agencies is crucial for tracking agreements, disputes, and promises. Use certified mail for better documentation of your communications with debt collectors.

Request a validation letter from the debt collector if they contact you and you haven’t received one to keep clear records of their claims. Maintaining professionalism in communications upholds your reputation and aids in resolving issues effectively.

Let’s now explore how obtaining witness statements can support your dispute.

Obtain Witness Statements

Witness statements can serve as a critical tool in supporting your dispute against a collection claim. These statements can bolster your case by confirming that you do not owe the claimed debt.

Now, let’s move on to drafting an effective debt dispute letter.

Drafting an Effective Debt Dispute Letter

A debt dispute letter is a formal letter disputing the validity or accuracy of a claimed debt. Your dispute letter should include your name, address, email, account number, date of writing, creditor’s details, a clear explanation of the dispute, and a request for proof documents. Articulate discrepancies clearly to make your case stronger.

Collecting supporting documents, such as bank statements and correspondence with creditors, is essential to substantiate your dispute. When disputing a credit report error, document specific inaccuracies, including account names, numbers, and the nature of the errors.

Let’s break down the key elements to include in your dispute letter.

Key Elements to Include

The dispute letter must have personal information, the debt amount, and a specific request for verification from the creditor. Clearly state the reasons for disputing the debt and include any supporting documents. By providing all necessary information, you make it easier for the creditor or collection agency to investigate and resolve the dispute.

Next, let’s review a sample debt dispute letter to help you draft your own.

Sample Debt Dispute Letter

A sample letter can serve as a useful reference for formatting and content when writing your own dispute letter. Including all required elements and presenting your case clearly increases the chances of a successful dispute.

Here are the best practices for sending your dispute letter.

Sending Your Dispute Letter

Send your dispute letter via certified mail with return receipt requested to document communications with debt collectors and provide proof of delivery. Dispatch the letter within 30 days of receiving a collection claim.

Sending the letter to the creditor or collection agency ensures your dispute is formally lodged and tracked. Now that your dispute letter is sent, here’s how to follow up on your dispute.

Following Up on Your Dispute

Disputing collections can help rectify inaccuracies that negatively affect credit scores. Keep a copy of the dispute letter and the certified mail receipt for your records. If a debt collector violates your rights, submit a complaint to the CFPB, state attorney general, or FTC.

Consumers can specify how and when debt collectors can contact them or cease communication. The follow-up process involves awaiting response, monitoring credit reports, and taking further action.

Awaiting Response

After disputing an error, monitor the situation closely, as credit bureaus typically have 30 days to conduct their investigation. Track any updates from the credit bureaus regarding your dispute.

Monitoring Credit Reports

Regularly monitor credit reports to ensure disputed items are removed or corrected promptly. Verifying the results of disputes helps assess the impact on your credit scores and financial health with the credit bureau.

Detailed records of all interactions with creditors help track agreements and disputes. If the dispute remains unresolved, here’s what to do next.

Taking Further Action

If your dispute remains unresolved, escalate the issue by filing complaints with consumer protection agencies such as the CFPB, state attorney general, or FTC.

Let’s discuss your rights as outlined in the Fair Debt Collection Practices Act (FDCPA).

Knowing Your Rights Under FDCPA

The Fair Debt Collection Practices Act (FDCPA) applies to debts primarily for personal, family, or household use. Debt collectors, including law firms that regularly collect debts, must adhere to the FDCPA. Debt collectors who abuse or threaten consumers violate the FDCPA and can be held accountable.

State laws may also provide protections against debt collection harassment beyond the FDCPA. Consumers can dispute debts with collectors at any time. If disputed within 30 days, debt collectors must stop contacting the consumer until they provide verification of the debt.

Let’s now discuss the statute of limitations on debt collections.

Statute of Limitations on Debt Collections

The statute of limitations on credit card debt varies by state, ranging from three to ten years. The statute of limitations on debt collections typically ranges from 3 to 15 years, determining how long a creditor or collection agency can legally pursue the debt through court action.

Even after the statute of limitations has expired, debt collectors may still attempt to collect on the debt. A ‘time-barred debt’ refers to a debt for which the statute of limitations has run out, making it no longer legally collectible through court actions.

Delinquent debts remain on a credit report for seven years, irrespective of whether the statute of limitations has expired.

Summary

In summary, disputing collections on your credit report is a critical step in maintaining your credit health. Whether it’s due to billing errors, identity theft, services not rendered, or incorrect account information, knowing how to gather evidence, draft an effective dispute letter, and follow up can make a significant difference. Understanding your rights under the FDCPA and the statute of limitations on debt collections further empowers you to take control of your financial future. Take these steps seriously, and you’ll be well on your way to a brighter financial outlook.

Frequently Asked Questions

What is a debt dispute letter?

A debt dispute letter is your powerful tool to challenge inaccuracies in a claimed debt by requesting verification from the creditor. Use it to take control of your financial situation!

How long does a debt collection stay on my credit report?

A debt collection can stay on your credit report for seven years, so take proactive steps now to improve your credit health moving forward!

What should I do if I suspect identity theft?

If you suspect identity theft, act swiftly by reporting it to the authorities and disputing any fraudulent debts with credit bureaus. Taking prompt action will help protect your identity and finances.

How do I send a dispute letter?

To effectively send your dispute letter, use certified mail with a return receipt requested for documentation and proof of delivery. This approach ensures your concerns are acknowledged and taken seriously!

What are my rights under the FDCPA?

You have the right to fair treatment under the FDCPA, allowing you to dispute debts and requiring collectors to halt contact until verification is provided if you dispute within 30 days. Stand firm in your rights and take control of your financial situation!